Three analysts have stepped up to the plate with estimates for this quarter predicting an average of .02 cents in 4Q. Only one predicted last quarter in 3Q missing by only .03 cents, which was better than the .07 & .08 cents consensus misses in quarters 1 & 2. It doesn’t statistically represent an improvement in accuracy (1 sample), but let’s hope so.

Interestingly, the 3 analysts consensus for FY 2009 is .10 cents. ENGlobal has earned only .07 cents in quarters 1-3 and a .02 cents average for 4Q yields .09 cents not the .10 as in their yearly prediction. Averages can work strangely as averages do. Regardless, the bottom line is a very poor year for 2009.

The four-quarter trailing PE is about to change drastically by -.13 cents. The 4Q ’08 of .15 cents will be replaced by an estimated .02 cents next quarter. What this will do to the next trailing PE ratio is literally cut ENG’s base divisible value from .22 cents to .09 or .10 cents (the latter being optimistic). This will be about a 60% drop, so beware. If you have researched ENG you haven’t seen any articles or analyst comments covering this aspect in the last year! I find this unusual.

Two analysts predict average revenue of 91.65M this quarter down from 136M 4Q last year. Remember also that they had hurricane Ike work helping last year. Due to this downturn sales growth is therefore estimated at –32.6%. Revenue FY ’09 is estimated at 353.78M or down –28.3% from 493.33M in FY ’08. The good news is growth is expected to be +11.2% next year. However, this is 11.2% up from this year’s negative –28.3% result, so we are going up less than half in 2010 of what we lost from last year. This will take time and refreshment in the management of operations to recover lost momentum.

In my last blog entry I used yearly earnings of .10 cents to calculate PE. That estimate seems pretty close now that analysts are predicting .02 in 4Q where I used .03 (on target if you use analyst’s yearly estimate). A gift PE of 15 at .09 cents yields $1.35 value per share - .10 cents yields $1.50 so there is your range for a PE of 15. If you use less than 15 the price goes down. This is why I haven’t liked the stock prospects near-term especially when the stock market has been running so high.

At this writing the DOW have moved up from ~8,100 this summer to over 10,400 without significant retracement or healthy pause! Moreover, it is up from 6,150 in March with a moderate pause/retracement this summer. Even in a healthy economy we would see some basing. In this bullish short-term Dow move ENG has dropped to ~$2.75 from peaks of $6 or $5 (take your pick) on poor earnings performance. IMHO, I think the hedge funds have supported the stock price. My concern is, that if ENG was and is being supported in a short-term Bull trend where is it going to go when the market corrects?

We have seen some profits in a few sectors and stock sellers (brokerages) are making a killing with thinned out competition and a rising market. However, if you poll all your friends what will the majority of them say of their personal well being? Consumers make up 70% of the economy. Jobs are still hemorrhaging. Sure, it is a lagging indicator – AFTER the turn, which has not appeared! Take a look at Job Losses from past recessions:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116091.jpg

Some more important indicators are Housing Sales:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116092.jpg

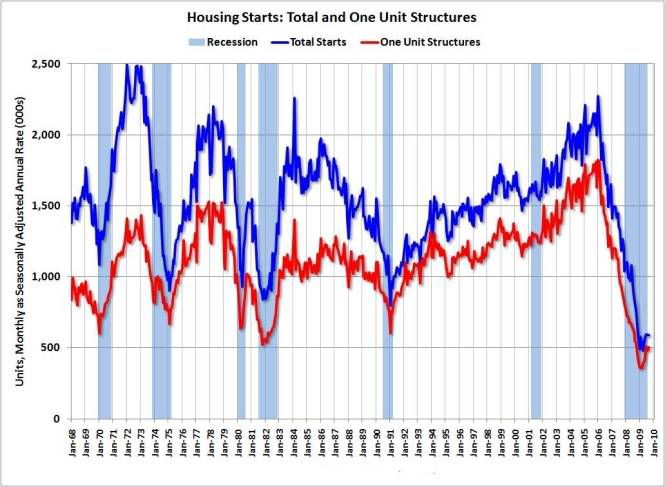

And, Housing Starts:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116093.jpg

Now read this short article about a Fed Governor’s speech:

http://www.reuters.com/article/topNews/idUSTRE5AF17U20091116?feedType=nl&feedName=ustopnewsearly

These are some reasons why I think the recession problems are not over by any means. The outlook is tenuous at best. The Obama administration and the media are trying to portray some level of success with the economy and with world travel before waving foreign crowds. In effect, nothing has really been done to create jobs.

So what’s going to happen? I pointed out in the last two blog entries that certain hedge funds have bought in and bought in at the wrong time. The stock will not stay even because there is no way for them to make money. I predicted a huge cash burn to support the stock price and we have actually gone down some. Cash is available (plentiful and cheap) to entities dealing in the stocks as per evident in the rising DOW and earnings reports. This will last as long as we see an overall upward trend but when it does turn south it will be bailout time.

Three analysts project .35 cents earning by ENGlobal for FY 2010. This average is on huge variation from .25 cents to .50 cents. With two negative –100% surprises in a row I am in ‘show me’ the earnings and better predictability mode. Will the stock trade on a forward-looking PE? First off, I don’t have much confidence with that much variation in next year's prediction. Just ask yourself the questions: Did it do this last year? Did it even trade on actual numbers? Regardless of how you balance the answers, the analysts and expectations were wrong – even in the Bullish move off an early spring bottom (even if so a bottom).

I get no pleasure reporting or predicting such an outlook. I have been bullish on and even accused of pumping ENGlobal stock for over 10 years. It ran from .50 cents to over $18 in that time and the potential was there to make money. I endeavored to simply tell the truth based on potential, numbers and trend. It just isn’t so good and even a poor outlook right now. Review the actual comments (bullet points) from the last CC in the 10 November 2009 blog entry. Or, listen to the archived recording. Management, albeit honest, is stating slow potential and a long recovery. It will take 1 to 2 yrs to get back to where we were based on management's comments, so don’t expect major positive moves on fundamental improvement. Major upward moves will be by other market forces.

I would expect to see more small acquisitions that are accretive to earnings and easy to fit in. This is an easy inorganic way to grow revenue and earnings. For an organic return to potential, which is more important, I look for two basic things. 1) A change in the management of operations (this is broad I know); and, 2) The fundamental basis of earning significant profits will have to be reestablished. This is how I believe ENGlobal will regain potential. Good luck to everyone.

27 November 2009

{kind=link}

{kind=link}

{kind=link}

10 November 2009

ENGlobal Corporation 3Q Analysis, Comments & 4Q Forward

(Beep) Houston, you have a problem!

The results are in. As predicted in the preceding blog post the downtrend prevailed to slightly negative earnings rounded officially to “breakeven” results. Yes, negative earnings ($69,000)! When was the last time that happened on operations outside of special events? Only one of four analysts estimated earnings and this was .03 cents. Therefore, we missed again on earnings and were 2 million shy on revenue. We had the similar breakeven results last quarter on slightly positive earnings. Still, no turnaround has occurred for ENG. And, like Apollo 13 they are headed in the wrong direction before a turnaround occurs. That turnaround is going to be a while and excruciating. I don’t see a good short-term picture so be prepared. All this is ‘pipeline’, as you may know, and inertia works the same in all directions. Management will have to make more changes.

What we have seen is a change in Business Development. Michael Harrison is the new chief there and seems to have a good pedigree. I hope he can recover lost business and develop new opportunities. I would hope to think he has targeted right in on too few IR (real) news reports. I have pointed this out for years, ad nausea. Frequent news items add confidence to investors, employees, and companies seeking work. I believe they promote business. It is also a counter to misrepresentation and manipulation. These are only a partial list of benefits from active business news reporting. We have new energy in BD; a positive change but ENGlobal’s problems are not entirely solved with this move. There is an operations problem in my opinion, from my background experience, that needs to be fixed. You can get all the business you want but if you can’t execute efficiently you will falter.

When it was announced some time ago that former CEO, Michael Burrow, was giving up COB to just being the CEO a lot of good reasons were released for dividing up those roles. What happened to those reasons and company attitude after Mike Burrow retired? I think much work was now laid on one set of eyes – top responsible management was cut in half. A lot of people can run a company during good times, but invariably it is more difficult during bad economic times, now at half the observing and managing brainpower.

I would change and bolster the whole top management structure. Better information has to reach the top level being reflective of what is going on in the trenches. I have seen this problem before in other companies without a senior President and/or COO. You need more sensing capability, especially in a bad economy.

As COO I made active use of my CFO and forensic accounting. A good CFO can advise and identify with almost crystal ball precision. This information, in turn, can be converted into objectives, goals and decisions. All Presidents should meet monthly with the CFO and review progress and projections. This is how you avoid trouble. If you don’t think this is an appropriate role for a CFO then you have a bad CFO that needs replacing. ENGlobal has a great CFO.

Lets look at the report and data:

First off, the title is brilliant – complete with caveat – great IR work. The data is not so good and the reason for the title.

- Breakeven earnings per diluted share, a decrease from $0.13. Third quarter net loss of $69,000 or $0.00.

- Revenue of $87.3 million, a decrease of 29%, with $7.6 million of the decrease due to a reduced level of pass-through procurement revenue. (The one analyst projected $89.3 million)

- Consolidated gross profit margin as a percentage of revenue of 8.2%, a decrease from 11.1%.

- Continued strong liquidity, with positive cash flow from operations of $4.5 million and $18.5 million for the three and nine months ended September 30, 2009, respectively.

- 65% reduction of total long-term debt to $11.8 million from $34.0 million.

- "Overall SG&A expenses decreased $0.5 million, or 6.3%, to $7.0 million for the three months ended September 30, 2009, from $7.5 million for the comparable prior-year period. The third quarter 2009 SG&A represents an increase of 3% compared to $6.8 million in the second quarter 2009. As a percentage of revenue, SG&A expense increased to 8.0% for the three months ended September 30, 2009, from 6.1% for the comparable prior year period."

Employees have decreased by at least 600 and only a 6.3% decrease in SG&A in Q3? This percentage down does not seem reasonable for amount of employees lost. If SG&A per billable hour were calculated you could see how inefficient and costly this is. Additionally, 3Q SG&A was up 3% over 2Q, and SG&A up YOY in 3Qs as a percentage of revenue? They added 100 employees in 3Q and SG&A went up 3%. I know there is more to this but earnings were a little worse 2Q to 3Q for the rise in SG&A and big time worse (.13) YOY - simply the wrong direction. I believe I know what they are doing buy some other comments made in the CC. They are purposely carrying more overhead (people) so they can ramp up faster in case of contract increase. It is still to much, especially when you understand the capital project outlook comments in the CC forthcoming.

The conference call was rather short, 15 minutes, excluding questions. Some memorable comments were:

- Work has “somewhat stabilized” during the second and third quarters of this year. Unfortunately, over this time period, we’ve seen about one-third lower levels of billable man hours than we enjoyed at the same time last year.

- Billable hours has trended “slowly upward”…. and starting to see the first inklings of turning up…. but still roughly down about 25% from our best levels of last year.

- What we are lacking is the large capital work in domestic downstream, and that’s why we are looking into new areas to replace this lost revenue.

- Recovery in 1H or 2H. Earnings will improve sometime next year depending on capital spending.

- There will be an extended time before capital projects coming back.*

* Bill Coskey: “I think what we are seeing right now from the domestic downstream area is deferred maintenance work. I don’t think we have seen any significant large capital work to speak of.”

“We are expecting an extended, I mean I am expecting an extended period of time of low capital spending in the domestic downstream inventory, a lot of that’s driven by and certainly created around Cap and Trade, and if you have an old plant and you are refining, why would you want to go make a big investment in it, if you have that sort of hanging over your head. And a lot of it relates to utilization of these facilities and margins and spreads.”

“So, there is not many positives out there right now for the processing business of large capital work, and that’s really what stimulates us to look at these other areas. And it will eventually come back as it always does, but I think it’s going to be an extended period of time before it does.”

At least this CC is more realistic compared to the last three CCs. There had been small warnings. However, I never heard anything that would have lead me to expect these results of the last three missed quarters. I almost get the sense the company is being managed down and not up. If you have run a company or a small conglomerate you will understand.

Debt has been paid down in a fantastic way. This is great especially when you need to borrow again or going to sell the company. But does that help you earn money? The answer is no. I’d still prefer no debt, but not over earnings. It is a separate issue and that is the point.

When you look into the breakdown of the quarter the Engineering group fell off the most followed by miniscule decreases (almost par) results from Construction and Land. Automation was the star in a bad quarter and commendation is deserved.

I need to make a point about Automation. It has high variability on earnings. ENGlobal has been providing some useful information the last few years about the individual company division performance. I take that information and crunch it a little beyond what normal investors or analysts do using a statistical package called ANOVA (ANalysis Of VAriance). I have used it in scientific and performance studies. Applying this to business is unconventional from original concept. However, it does reveal where variance is, precisely. It identifies a certain type of problem in business – reliability of performance as compared to other entities. I ran it on Land, Engineering, Construction and Automation.

Land came out good. Construction came out OK – some variations, presumably overhead and job fluctuation. Engineering showed variation that is accountable by loss of work/employees. Other than that Engineering seems OK despite overhead. Note: It is unaccountable variation that is the real issue.

Automation earnings variation is all over the map. Since I respect the leadership there I have to then question middle management and what information they are using/not using with regards to their management practices. They actually boosted earnings this quarter and that is to be considered when looking at the whole quarter. With high variability comes the question, what will happen in future quarters?

Where is the stock price going to go? Consider that 2Q and 3Q are ENGlobal’s strongest quarters in the year and we got only breakeven results earning nothing. The markets have generally risen huge since the summer with no healthy retrace and basing. ENG has not benefited with participation in the run up but that is not to say it hasn’t benefited in support of its pricing at $4 range and now $3 range. With unemployment still not improving and extension upon extension of employment benefits, I think markets will fall in the future. This is important because where do you think things will go on these bad earnings in a falling or correcting market?

Hedge funds and institutions are not in a good position. Earnings are bad with a weak and iffy outlook. Short interest is down, so there is no real money to be made from a down game. Look at what happened in 2Q with terrible earnings. It looked to me like ENGlobal was propped up and supported for a long time in the $4 range on the bad news. By most accounts it should have been lower. Then, when the wind blew after 3Q finished and in late October, hello $3s. Did you enjoy Friday’s stock action before earnings? Did you see the heavy volume in the low $3s, a sudden run up about .50 on low volume quickly, then closing at $3.42? Three words – Hedge Funds, Manipulation. Now we have no good news to lift the price. It is going to be interesting – the support cash burn should be incredible. Expect more post and “news” pumping on weak analysis. If the analysis weren’t weak I wouldn’t call it pumping or bashing.

We have a long time until the next 4Q earnings report. That should come in mid March. 4Q is usually ENGlobal’s weakest quarter in which low billable hours occur during the holidays. Accounting adjustments are made in this period also. Last year was an exception to the usual low income; they had hurricane Ike work that pumped in huge money. No Ike this year.

Presently we have 3 quarters 2009 and earning only 7 cents. How are we going to predict a fair price with PE? What will 4Q yield? Last post I came up with $2.55 on apparently now over-optimistic theoretical numbers – 3 cents for 3Q (now known to be zero) and 7 cents 4Q. I have little confidence to speculate a number. But if we earned 3 cents in 4Q for total of .10 cents for the year plus a being kind 15 PE, this yields $1.50. Does this sound as bad to you as it does to me? I am hoping there will be market good will and way forward looking expectations. It all hinges on management quality and their decisions.

I will hold the shares I have. I would observe for management changes first and then real improving results before buying. This is a realistic view considering the long recovery period ahead. Good luck to everyone.

04 November 2009

ENGlobal Corporation 3Q and Forward

It has been a long time since I last posted while trying to get a sense of ENGlobal’s direction. Moreover, determining what is affecting the downturn of the stock, the economy and/or management. I have been about as bullish as anyone can be for the last 10 years. I have been honest about the potential I saw from below .50 cents to an all time high of over $18. The bashers were wrong and had their own agendas, for if you followed their advice you would have not had the potential of making money in ENG’s past long-term rise.

That said, observing results and listening to comments in CCs and releases over the last year I do not like the trend. Especially the information. Long-term I have confidence ENG will grow back. They fill the needs of an oil dependent world and other areas ENG is expanding into. Short-term has been and is awful. For the last 5 quarters we have had surprise earnings all of them massive up or down.

2Q ’08 huge up, euphoria reigned, CC comments were “ENG will meet or exceed in 3Q ’08 compared to second quarter”. The economy cratered and right in the midst, at the worst possible time ENG warns and then performs 11 cents short. The 3Q ’08 CC was more reserved and less bullish. Investor’s I know came away feeling from information related that hurricane Ike was mostly to blame. Not so in my opinion. Four loss areas were discussed with varied emphasis, the hurricane being one of them. However, I can tell you from both rough and detailed calculations I made that the hurricane losses were only about 2 of those 11 cents. That leaves 9 cents of management related miss. Remember, we were warned rather late too, that is indicative.

After a long period with little affecting news came 4Q ’08 earnings in March ’09 with some moderate upward surprise, mostly due to hurricane repair work. Investors still in shock over the markets and the last quarter were little impressed. In that CC one would think ENG’s problems had settled down but there was some warning that ENGlobal was not immune to the economy. The later was proved with analysts’ missing by 7 cents in 1Q ’09. Then this CC led me to believe that the problems had leveled off and things were going to improve. Wrong again. 2Q ’09 came in with “breakeven” results. Now this is excellent IR phrasing for other news agencies picking up the story – actually brilliant. Let me rephrase 2Q ’09 in actual numbers: ENGlobal missed by 8 cents. That is terrible, simply speaking.

How did the press react? Not negatively and that was unusual. Some history: Remember in the past when Sidoti raised their estimate days before earnings in a 3Q? This was enough to raise the consensus estimate and in effect cause a technical miss by a penny on diluted shares (on target with basic shares). Results were actually an upward surprise by a penny over Sidoti’s previous estimate on basic shares. IMHO, someone did not want that good news. What story did all the business news announced? There was huge negative press over a penny miss on one analyst‘s questionable action. One penny then, so why was this massive 8-cent miss less attacked? One, the wording was better. Two, also with the earnings release came the announcement of a small acquisition. I understand “small” as less than 20 people and the actual number of gained employees wasn’t released - so you know it was small as described. Nevertheless, this got unusual positive play with an unusual (for ENGlobal release rates) follow-up news release ten days later that the acquisition was completed and integrated. Again, it confirms being small with the short period of completion.

Back to the question, why did the media seemingly pump this news and less severe about the 8 cent loss? Three, short interest was way down so no “down game” from hedge funds is a possible theory. Then I saw an old institutional owner Jeff Gendell and Tontine had bought back into ENG! Check institutional ownership. Could this be reason number four?

http://www.zerohedge.com/article/guest-post-jeffrey-gendells-hedge-fund-tontine-associates-rebirth

There is no proof outside of witnessing but last time Gendell/Tontine got in and during his ownership tenure strange things happened to the stock. Unusual pumping and negatives from press, one particular analyst and public forums. Sidoti started covering ENG soon after Gendell originally bought in. I note there are additional hedge funds that own significant shares, therein lies more potential, even competitive manipulation. Anyone that thinks hedge funds act fairly within a fair market should not invest. (See the Cramer hedge fund confession video in a previous post.)

Now with Tontine entering the picture again we have unusual positive handling by the press. Remember, at this point there is insignificant short interest. Then came along an article by The Fool dot com:

http://www.fool.com/investing/dividends-income/2009/08/24/fearful-stocks-for-greedy-investors.aspx

They are generally respected and usually write good articles with fair factual coverage. Before I knew the powerful Gendell/Tontine entered the stock again I could not understand the aforementioned positive press and now an actual pumping article about ENG. The whole basis of the Fool article was what a price deal it was based on WAY past earnings without mention of the several recent terrible quarters and trend. Moreover, in the past they have delved into management analysis and how this relates to results, but not so in this article. I know and like ENG very much but this was a biased favoring pump. The 2Q ’09 CC, again, offered more of the same feeling that the problems are behind us with a slow but improving picture. Metrics were offered this time, but with no comparing references they are soothing at best.

I have believed ENG has suffered manipulation in the past and now. I have made trades that were seemingly countered beyond logical account on too many occasions. Other investors, brokers and past ENGlobal management have reported the same to me. I have more information presently to consider besides unusual behavior and constant Level 2 observations I made in the past. I knew a sophisticated computer Algorithmic Trading programs that appears to sense all the major markets inputs was in play. I even discussed this with a NASDAQ representative who agreed it happens on the NASDAQ. What I found later and this representative did not tell me was that Flash Trading was being sold as subscription by the NASDAQ and other markets. Look it up on Wikipedia and in Google.

http://en.wikipedia.org/wiki/Flash_trading

http://www.reuters.com/article/businessNews/idUSTRE59Q21B20091027?feedType=nl&feedName=usbusinessearly

http://en.wikipedia.org/wiki/Algorithmic_trading

You will be appalled at what Flash Trading does, and that the SEC is slow to act on this. Basically, it gives a subscribing customer a split second advantage to know what Bids and Asks are being placed before what the public knows. In a sense it is a private pre-market. With this Flash information tied into a computer program the computer can then counter any undesired effect (within certain and most common volumes). All of this is done at speeds just below the speed of light. I ask you - does not this make you mad? Isn’t this a fair market removed? The SEC is supposedly trying to correct this.

Also consider Dark Pool trading. It is a means whereby institutions can operate under cover without exposing their moves. Again, this is outside of what investors are supposed to know according to SEC rules and fair markets.

http://en.wikipedia.org/wiki/Dark_pools_of_liquidity

http://www.reuters.com/article/businessNews/idUSTRE59Q0QP20091027?feedType=nl&feedName=usbeforethebell

We all know what hedge funds will do and use any information they can get to their (unfair) advantage. Anyone I know who trades ENG (as well as other stocks) and uses Level 2 will come to agreement that manipulation occurs. This doesn’t mean you can’t make money. If you play the moves right you can profit. But the program operators know what they want to do and will do ahead of time. ENG’s performance in the past made it easier to make money because they were trending up with staged level offs. The recent downtrend makes it difficult to know what is going to happen near-term, more so with hedge funds doing their thing. I am not expecting good news 3Q ’09, results could be negative. The trend is down and past CC “guidance” has not represented later results. I won’t be over critical because I would try to paint the best possible picture fairly and fair is always debatable. However, you may decide for yourselves by listening to the archived CCs and news releases compared to actual performance and numbers reported. It is all there.

ENG has lost two analysts since last year’s disappointment. Sidoti was one and I don’t miss their biased performance and questions. By the way, Sidoti dropped coverage after Gendell previously dumped ENG. At the moment Gendell/Tontine is the number one stockholder outside of ENGlobal’s CEO, Bill Coskey. As of this writing only one analyst has an estimate of 3 cents for this quarter. ENG missed by 7 cents in 1Q, earning 7 and missed by 8 cents 2Q, thus earning only 7 cents in 1H ’09. We have a 3-cent estimate on 3Q and no estimate for 4Q (can’t blame analysts there). It makes it hard to calculate PE but when you use estimates and educated guesses you can come up with some pretty bad stock prices. 1H - 7 cents plus 3Q’s 3 cents, plus say a relatively good 7 cents in 4Q = 17 cents. Multiply a 15 PE (bad economy) and it yields $2.55. Consider manipulating effects you can have an idea of the possible range.

In the past, I have discussed how I handle PE and I believe I am being consistent with my use in bad and good markets. It just isn’t pretty. At some point the trend will change. I know ENG has lost a significant amount of employees. So have a lot of companies all over the world. I can’t be certain of the numbers so I won’t discuss it, but it does affect billable hours. There was some significant extra money on the 1Q balance sheet I could not account for. This could show up anytime this year, especially as an acquisition. ENGlobal will turn around. How long it will be I have no idea. I can’t tell with recent past and current information. I sold most of my stock and hold a core position. Opportunity waits at some point. That’s the view from my cockpit. You are flying your own aircraft. Good luck to everyone.

That said, observing results and listening to comments in CCs and releases over the last year I do not like the trend. Especially the information. Long-term I have confidence ENG will grow back. They fill the needs of an oil dependent world and other areas ENG is expanding into. Short-term has been and is awful. For the last 5 quarters we have had surprise earnings all of them massive up or down.

2Q ’08 huge up, euphoria reigned, CC comments were “ENG will meet or exceed in 3Q ’08 compared to second quarter”. The economy cratered and right in the midst, at the worst possible time ENG warns and then performs 11 cents short. The 3Q ’08 CC was more reserved and less bullish. Investor’s I know came away feeling from information related that hurricane Ike was mostly to blame. Not so in my opinion. Four loss areas were discussed with varied emphasis, the hurricane being one of them. However, I can tell you from both rough and detailed calculations I made that the hurricane losses were only about 2 of those 11 cents. That leaves 9 cents of management related miss. Remember, we were warned rather late too, that is indicative.

After a long period with little affecting news came 4Q ’08 earnings in March ’09 with some moderate upward surprise, mostly due to hurricane repair work. Investors still in shock over the markets and the last quarter were little impressed. In that CC one would think ENG’s problems had settled down but there was some warning that ENGlobal was not immune to the economy. The later was proved with analysts’ missing by 7 cents in 1Q ’09. Then this CC led me to believe that the problems had leveled off and things were going to improve. Wrong again. 2Q ’09 came in with “breakeven” results. Now this is excellent IR phrasing for other news agencies picking up the story – actually brilliant. Let me rephrase 2Q ’09 in actual numbers: ENGlobal missed by 8 cents. That is terrible, simply speaking.

How did the press react? Not negatively and that was unusual. Some history: Remember in the past when Sidoti raised their estimate days before earnings in a 3Q? This was enough to raise the consensus estimate and in effect cause a technical miss by a penny on diluted shares (on target with basic shares). Results were actually an upward surprise by a penny over Sidoti’s previous estimate on basic shares. IMHO, someone did not want that good news. What story did all the business news announced? There was huge negative press over a penny miss on one analyst‘s questionable action. One penny then, so why was this massive 8-cent miss less attacked? One, the wording was better. Two, also with the earnings release came the announcement of a small acquisition. I understand “small” as less than 20 people and the actual number of gained employees wasn’t released - so you know it was small as described. Nevertheless, this got unusual positive play with an unusual (for ENGlobal release rates) follow-up news release ten days later that the acquisition was completed and integrated. Again, it confirms being small with the short period of completion.

Back to the question, why did the media seemingly pump this news and less severe about the 8 cent loss? Three, short interest was way down so no “down game” from hedge funds is a possible theory. Then I saw an old institutional owner Jeff Gendell and Tontine had bought back into ENG! Check institutional ownership. Could this be reason number four?

http://www.zerohedge.com/article/guest-post-jeffrey-gendells-hedge-fund-tontine-associates-rebirth

There is no proof outside of witnessing but last time Gendell/Tontine got in and during his ownership tenure strange things happened to the stock. Unusual pumping and negatives from press, one particular analyst and public forums. Sidoti started covering ENG soon after Gendell originally bought in. I note there are additional hedge funds that own significant shares, therein lies more potential, even competitive manipulation. Anyone that thinks hedge funds act fairly within a fair market should not invest. (See the Cramer hedge fund confession video in a previous post.)

Now with Tontine entering the picture again we have unusual positive handling by the press. Remember, at this point there is insignificant short interest. Then came along an article by The Fool dot com:

http://www.fool.com/investing/dividends-income/2009/08/24/fearful-stocks-for-greedy-investors.aspx

They are generally respected and usually write good articles with fair factual coverage. Before I knew the powerful Gendell/Tontine entered the stock again I could not understand the aforementioned positive press and now an actual pumping article about ENG. The whole basis of the Fool article was what a price deal it was based on WAY past earnings without mention of the several recent terrible quarters and trend. Moreover, in the past they have delved into management analysis and how this relates to results, but not so in this article. I know and like ENG very much but this was a biased favoring pump. The 2Q ’09 CC, again, offered more of the same feeling that the problems are behind us with a slow but improving picture. Metrics were offered this time, but with no comparing references they are soothing at best.

I have believed ENG has suffered manipulation in the past and now. I have made trades that were seemingly countered beyond logical account on too many occasions. Other investors, brokers and past ENGlobal management have reported the same to me. I have more information presently to consider besides unusual behavior and constant Level 2 observations I made in the past. I knew a sophisticated computer Algorithmic Trading programs that appears to sense all the major markets inputs was in play. I even discussed this with a NASDAQ representative who agreed it happens on the NASDAQ. What I found later and this representative did not tell me was that Flash Trading was being sold as subscription by the NASDAQ and other markets. Look it up on Wikipedia and in Google.

http://en.wikipedia.org/wiki/Flash_trading

http://www.reuters.com/article/businessNews/idUSTRE59Q21B20091027?feedType=nl&feedName=usbusinessearly

http://en.wikipedia.org/wiki/Algorithmic_trading

You will be appalled at what Flash Trading does, and that the SEC is slow to act on this. Basically, it gives a subscribing customer a split second advantage to know what Bids and Asks are being placed before what the public knows. In a sense it is a private pre-market. With this Flash information tied into a computer program the computer can then counter any undesired effect (within certain and most common volumes). All of this is done at speeds just below the speed of light. I ask you - does not this make you mad? Isn’t this a fair market removed? The SEC is supposedly trying to correct this.

Also consider Dark Pool trading. It is a means whereby institutions can operate under cover without exposing their moves. Again, this is outside of what investors are supposed to know according to SEC rules and fair markets.

http://en.wikipedia.org/wiki/Dark_pools_of_liquidity

http://www.reuters.com/article/businessNews/idUSTRE59Q0QP20091027?feedType=nl&feedName=usbeforethebell

We all know what hedge funds will do and use any information they can get to their (unfair) advantage. Anyone I know who trades ENG (as well as other stocks) and uses Level 2 will come to agreement that manipulation occurs. This doesn’t mean you can’t make money. If you play the moves right you can profit. But the program operators know what they want to do and will do ahead of time. ENG’s performance in the past made it easier to make money because they were trending up with staged level offs. The recent downtrend makes it difficult to know what is going to happen near-term, more so with hedge funds doing their thing. I am not expecting good news 3Q ’09, results could be negative. The trend is down and past CC “guidance” has not represented later results. I won’t be over critical because I would try to paint the best possible picture fairly and fair is always debatable. However, you may decide for yourselves by listening to the archived CCs and news releases compared to actual performance and numbers reported. It is all there.

ENG has lost two analysts since last year’s disappointment. Sidoti was one and I don’t miss their biased performance and questions. By the way, Sidoti dropped coverage after Gendell previously dumped ENG. At the moment Gendell/Tontine is the number one stockholder outside of ENGlobal’s CEO, Bill Coskey. As of this writing only one analyst has an estimate of 3 cents for this quarter. ENG missed by 7 cents in 1Q, earning 7 and missed by 8 cents 2Q, thus earning only 7 cents in 1H ’09. We have a 3-cent estimate on 3Q and no estimate for 4Q (can’t blame analysts there). It makes it hard to calculate PE but when you use estimates and educated guesses you can come up with some pretty bad stock prices. 1H - 7 cents plus 3Q’s 3 cents, plus say a relatively good 7 cents in 4Q = 17 cents. Multiply a 15 PE (bad economy) and it yields $2.55. Consider manipulating effects you can have an idea of the possible range.

In the past, I have discussed how I handle PE and I believe I am being consistent with my use in bad and good markets. It just isn’t pretty. At some point the trend will change. I know ENG has lost a significant amount of employees. So have a lot of companies all over the world. I can’t be certain of the numbers so I won’t discuss it, but it does affect billable hours. There was some significant extra money on the 1Q balance sheet I could not account for. This could show up anytime this year, especially as an acquisition. ENGlobal will turn around. How long it will be I have no idea. I can’t tell with recent past and current information. I sold most of my stock and hold a core position. Opportunity waits at some point. That’s the view from my cockpit. You are flying your own aircraft. Good luck to everyone.

12 January 2009

ENGlobal Corporation Growing and 4Q Comments

Due to ENGlobal's rapidly growing business and healthy backlog ENG operations require more space. On 22 December an article appeared indicating ENGlobal's commitment for over 80,000 sq. ft. of additional space.

http://www.costar.com/News/Article.aspx?id=9EFAC239740BC9C886DE294CCF91934D&ref=1&src=rss

That project appears to be well underway. Before the article was written the expansion plans had already been submitted for permitting. Also, the invitation for subcontractors has been advertised and the bid date deadline has already past. You can see the Overall floor plan for the expansion project above. Click on the image for a closer view.

You may view the sub links to the plans and invitation for bids from subcontractors at this link. Drilling into the plan link you can view a .zip file of the entire set of plans.

http://www.costar.com/News/Article.aspx?id=9EFAC239740BC9C886DE294CCF91934D&ref=1&src=rss

That project appears to be well underway. Before the article was written the expansion plans had already been submitted for permitting. Also, the invitation for subcontractors has been advertised and the bid date deadline has already past. You can see the Overall floor plan for the expansion project above. Click on the image for a closer view.

You may view the sub links to the plans and invitation for bids from subcontractors at this link. Drilling into the plan link you can view a .zip file of the entire set of plans.

Based on my previous trips I believe this is ENG Automation's Houston Fabrication Unit moving into a newer, larger and more efficient HQ/Fabrication building. I reported in my last Annual Report to Stockholders that I saw this shop literally filled to the brim with contract work. I also think that the profit from the witnessed heavy contract load will add to other automation work momentum mentioned in previous posts for a very good 4Q. Additionally, EAG has a very high profit margin. I have seen advertisements from EAG and ENG's Land Group looking for new employees since early Fall to Present.

From previous company statements EAG and ELG are growing and I believe EAG is benefiting from earlier, albeit, nebulous contract announcements. Despite the hit ENG took from hurricane losses I think they will recoup much more in revenue and margins from damage repair and associated overtime in 4Q/1Q 2009. Remember, that from recent company statements increasing performance was expected not only from these two groups but also some from the Engineering and Construction Groups.

Despite the losses from hurricane and other company mentioned areas in the 3Q the continuing operations numbers range were indicative of great company health. Increasing in fact. Continuing operations is and will be the best measure of a company; it is a Wall Street standard. In 3Q the analysis showed ENGlobal’s continuing operations was .23-.25 cents per share. This would have been another company quarterly record and quite possibly an overall record without the write downs. Will there be more write downs? I can’t predict that and I would like any critic to document their specific special event/write down prediction categories and amounts with their criticism. Since special events occur infrequently, hence, the reliance on continuing operations.

In this terrible economy where does ENGlobal stand since the overall equity downturn. After the downturn was well underway ENG reported a measurable three quarter’s profit of .51 cents – 25% Higher than 2007. Backlog was 15% Higher. Billable was hours Up 20%. A 10 to 12 cent reduction in 3Q EPS due to special items indicate by adding this to the reported earnings of .13 yields a continuing operations EPS of .23 to .25 cents in Q3 2008. This represents an increase of 65 – 79% in continuing operations compared to Q3 2007. Given the actual past performance and positives given by the company ENGlobal should have a great 4Q. Moreover, based on already reported profit the headline for the 4Q/FY2008 will indicate a huge record year. How many companies do you see reporting good earnings and growth this these days?

Subscribe to:

Comments (Atom)