Three analysts have stepped up to the plate with estimates for this quarter predicting an average of .02 cents in 4Q. Only one predicted last quarter in 3Q missing by only .03 cents, which was better than the .07 & .08 cents consensus misses in quarters 1 & 2. It doesn’t statistically represent an improvement in accuracy (1 sample), but let’s hope so.

Interestingly, the 3 analysts consensus for FY 2009 is .10 cents. ENGlobal has earned only .07 cents in quarters 1-3 and a .02 cents average for 4Q yields .09 cents not the .10 as in their yearly prediction. Averages can work strangely as averages do. Regardless, the bottom line is a very poor year for 2009.

The four-quarter trailing PE is about to change drastically by -.13 cents. The 4Q ’08 of .15 cents will be replaced by an estimated .02 cents next quarter. What this will do to the next trailing PE ratio is literally cut ENG’s base divisible value from .22 cents to .09 or .10 cents (the latter being optimistic). This will be about a 60% drop, so beware. If you have researched ENG you haven’t seen any articles or analyst comments covering this aspect in the last year! I find this unusual.

Two analysts predict average revenue of 91.65M this quarter down from 136M 4Q last year. Remember also that they had hurricane Ike work helping last year. Due to this downturn sales growth is therefore estimated at –32.6%. Revenue FY ’09 is estimated at 353.78M or down –28.3% from 493.33M in FY ’08. The good news is growth is expected to be +11.2% next year. However, this is 11.2% up from this year’s negative –28.3% result, so we are going up less than half in 2010 of what we lost from last year. This will take time and refreshment in the management of operations to recover lost momentum.

In my last blog entry I used yearly earnings of .10 cents to calculate PE. That estimate seems pretty close now that analysts are predicting .02 in 4Q where I used .03 (on target if you use analyst’s yearly estimate). A gift PE of 15 at .09 cents yields $1.35 value per share - .10 cents yields $1.50 so there is your range for a PE of 15. If you use less than 15 the price goes down. This is why I haven’t liked the stock prospects near-term especially when the stock market has been running so high.

At this writing the DOW have moved up from ~8,100 this summer to over 10,400 without significant retracement or healthy pause! Moreover, it is up from 6,150 in March with a moderate pause/retracement this summer. Even in a healthy economy we would see some basing. In this bullish short-term Dow move ENG has dropped to ~$2.75 from peaks of $6 or $5 (take your pick) on poor earnings performance. IMHO, I think the hedge funds have supported the stock price. My concern is, that if ENG was and is being supported in a short-term Bull trend where is it going to go when the market corrects?

We have seen some profits in a few sectors and stock sellers (brokerages) are making a killing with thinned out competition and a rising market. However, if you poll all your friends what will the majority of them say of their personal well being? Consumers make up 70% of the economy. Jobs are still hemorrhaging. Sure, it is a lagging indicator – AFTER the turn, which has not appeared! Take a look at Job Losses from past recessions:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116091.jpg

Some more important indicators are Housing Sales:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116092.jpg

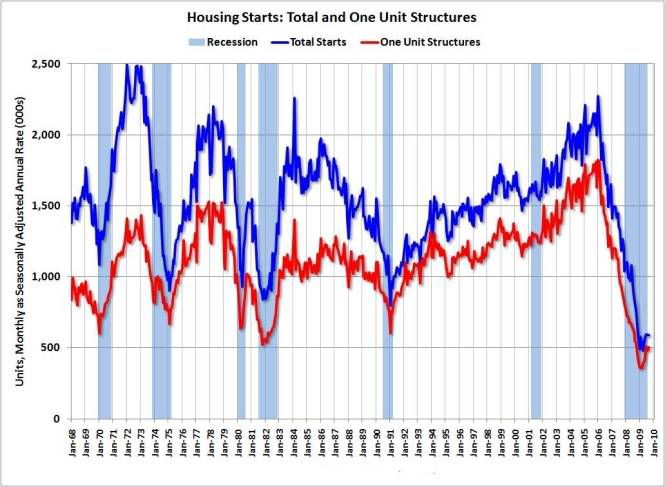

And, Housing Starts:

http://i418.photobucket.com/albums/pp267/t38pilot8202/1116093.jpg

Now read this short article about a Fed Governor’s speech:

http://www.reuters.com/article/topNews/idUSTRE5AF17U20091116?feedType=nl&feedName=ustopnewsearly

These are some reasons why I think the recession problems are not over by any means. The outlook is tenuous at best. The Obama administration and the media are trying to portray some level of success with the economy and with world travel before waving foreign crowds. In effect, nothing has really been done to create jobs.

So what’s going to happen? I pointed out in the last two blog entries that certain hedge funds have bought in and bought in at the wrong time. The stock will not stay even because there is no way for them to make money. I predicted a huge cash burn to support the stock price and we have actually gone down some. Cash is available (plentiful and cheap) to entities dealing in the stocks as per evident in the rising DOW and earnings reports. This will last as long as we see an overall upward trend but when it does turn south it will be bailout time.

Three analysts project .35 cents earning by ENGlobal for FY 2010. This average is on huge variation from .25 cents to .50 cents. With two negative –100% surprises in a row I am in ‘show me’ the earnings and better predictability mode. Will the stock trade on a forward-looking PE? First off, I don’t have much confidence with that much variation in next year's prediction. Just ask yourself the questions: Did it do this last year? Did it even trade on actual numbers? Regardless of how you balance the answers, the analysts and expectations were wrong – even in the Bullish move off an early spring bottom (even if so a bottom).

I get no pleasure reporting or predicting such an outlook. I have been bullish on and even accused of pumping ENGlobal stock for over 10 years. It ran from .50 cents to over $18 in that time and the potential was there to make money. I endeavored to simply tell the truth based on potential, numbers and trend. It just isn’t so good and even a poor outlook right now. Review the actual comments (bullet points) from the last CC in the 10 November 2009 blog entry. Or, listen to the archived recording. Management, albeit honest, is stating slow potential and a long recovery. It will take 1 to 2 yrs to get back to where we were based on management's comments, so don’t expect major positive moves on fundamental improvement. Major upward moves will be by other market forces.

I would expect to see more small acquisitions that are accretive to earnings and easy to fit in. This is an easy inorganic way to grow revenue and earnings. For an organic return to potential, which is more important, I look for two basic things. 1) A change in the management of operations (this is broad I know); and, 2) The fundamental basis of earning significant profits will have to be reestablished. This is how I believe ENGlobal will regain potential. Good luck to everyone.

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment